Two Bubbles, One on Top of the Other

This article was originally published in November 2025 under the title "The AI Industrial Transformation: Why This Bubble Has Real Revenue (Unlike the Dot-Com Fantasy)." The data was six months stale, and in this market six months changes everything. Rewritten with current numbers and a sharper thesis.

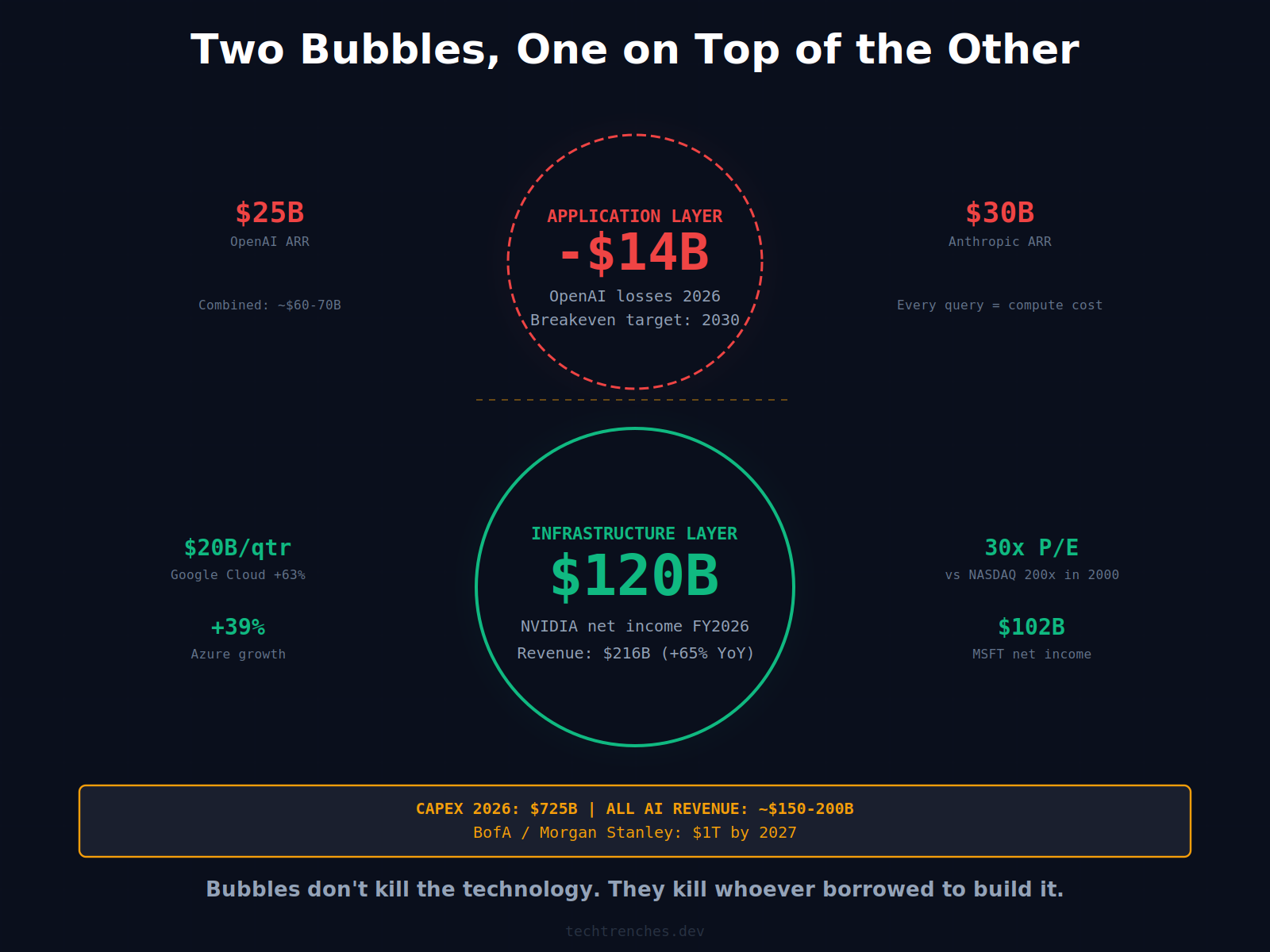

NVIDIA posted $216 billion in revenue for fiscal 2026. Net income: $120 billion. The data center division alone generated $194 billion. One chipmaker now earns more than most countries produce.

Everyone looks at that number and says the same thing: this isn’t 2000. The revenue is real. The infrastructure is real. The bubble has substance underneath it.

They’re half right. There is substance. But it’s in the wrong layer.

The AI economy is two bubbles stacked on top of each other. The infrastructure layer prints money. The application layer burns it. The dot-com had one layer. This has two. That structural difference determines what survives the correction.

The Infrastructure Layer Prints Money

Google Cloud hit $20 billion in Q1 2026, up 63% year over year. Microsoft Azure grew 39%. AWS remains the largest cloud provider. Microsoft alone posted $102 billion in net income for fiscal 2025. NVIDIA trades at roughly 30x forward earnings. At the dot-com peak, the NASDAQ Composite traded at 200x. Cisco alone hit over 400x.

Jerome Powell made the point himself in late 2025: unlike the dot-com companies, these firms actually have earnings. So it’s a different thing.

He’s right. But “different” can mean “better” or it can mean the failure mode is just harder to see. To see it, you have to look at the other layer.

The Application Layer Burns Cash

OpenAI hit $25 billion in annualized revenue by early 2026. Nine hundred million weekly users. Fifty million subscribers.

It also projects $14 billion in losses this year, targets breakeven by 2030, and has committed to roughly $600 billion in compute spending by the end of the decade.

Anthropic reportedly passed $30 billion in ARR by April 2026, growing from $1 billion fifteen months earlier. But Anthropic’s path to positive free cash flow is 2027 at the earliest, and that projection assumes growth rates that have never been sustained at this scale.

The core problem is inference economics. Traditional software has near-zero marginal cost: build it once, serve a million users. AI inference scales linearly. Every 10,000 users cost the same as the previous 10,000. Every query burns compute. There is no point where revenue growth outpaces cost growth by default, because serving the next customer costs the same as serving the last one. This breaks the fundamental SaaS assumption that scale creates margin.

The products work. Hundreds of millions of people use them daily, which is exactly why the economics are so strange. That scale of adoption still doesn’t close the books. Every new capability requires more compute, more infrastructure, more capital.

And the bill is about to land on the customer.

The Subsidy Is Ending

For two years, AI companies sold tokens below cost to build market share. The cloud playbook: get users dependent, then raise prices once switching costs are too high.

That phase is over. AI software fees increased 20-37% over the past year, according to spend management firm Tropic. Anthropic doubled its per-developer token costs from $6 to $13 per active day. OpenAI expects to lose 35 million subscribers on its $20/month plan, replacing them with 109 million users at $8/month on ChatGPT Go. The math works only if volume replaces margin.

The price increases aren’t always visible. Anthropic’s Opus 4.7, released in April 2026, ships with a new tokenizer that generates up to 35% more tokens for the same input text. The per-token price didn’t change. The number of tokens per request did. Some developers are reporting bills 47% higher on identical prompts. The price card says “unchanged.” The invoice says otherwise.

I watch this from both sides. We build AI integrations for clients. We also pay the token bills. A year ago, a simple RAG pipeline with 2-3 API calls was cheap enough that nobody tracked consumption. Today, complex multi-step agent workflows with 5-7 model calls cost real money, and the costs are trending up, not down.

There’s a real objection here: GPT-4 class output costs a fraction of what it did in 2023. That’s real. But it doesn’t show up on enterprise invoices the way you’d expect. As models get cheaper per token, companies use more tokens. Agent workflows chain 10-20 calls where a single prompt used to suffice. The cost per task drops. The number of tasks explodes. The bill goes up.

Uber’s CTO blew through his entire 2026 AI budget in weeks. A four-person startup spent $113,000 on AI in a single month. An NVIDIA VP said publicly that for his team, compute costs now exceed employee salaries. KPMG estimates businesses will nearly double their AI spending in the next year, averaging over $200 million each.

The companies that cut headcount assuming AI would fill the gap are discovering what the math actually looks like. The era of subsidized pricing is ending exactly when enterprises are scaling up.

Application layer burns cash, subsidies are ending, customers are getting squeezed. What does history say happens next?

The Dot-Com Had One Layer. This Has Two.

This is not 2000. Pets.com burned through $300 million in capital on less than $6 million in annual revenue. OpenAI has $25 billion in revenue and $14 billion in losses. The scale is different by four orders of magnitude. The structural problem is the same: spending exceeds income.

But in 1999, there was no profitable infrastructure layer underneath the bubble. Telecom companies spent $500 billion laying fiber, funded by debt. The startups burning cash on top of that fiber had no revenue. When the bubble popped, both layers collapsed. The fiber went dark. The startups went bankrupt.

Today the infrastructure layer is profitable. The hyperscalers fund most of their spending from operating cash flow. When I say “most,” I mean that was true in 2024 and early 2025. It’s becoming less true every quarter.

In 2025, hyperscalers issued $121 billion in bonds, more than four times the five-year average. Oracle’s credit default swaps widened to levels not seen since 2009. Alphabet priced a 100-year bond. Amazon’s free cash flow cratered from $38 billion to $11 billion as capex surged. I covered the free cash flow collapse in detail in the $650B sequel.

The infrastructure layer is shifting from cash-funded to debt-funded. Debt is what turned the telecom bubble from a boom into a bust. Not the applications failing. The infrastructure costs exceeding the infrastructure profits.

The question is how close we are to that threshold.

Where the Correction Hits

Goldman Sachs answered that question in December 2025: AI capex would need to reach $700 billion in 2026 to match the telecom peak as a proportion of GDP. As of the latest earnings calls, the four largest hyperscalers plan to spend $725 billion this year. Goldman’s scenario is no longer a forecast. It’s the baseline.

The application layer needs to generate enough revenue to justify the infrastructure layer’s investment. OpenAI is at $25 billion. Anthropic is at $30 billion. Add the smaller players and the foundation model sector generates perhaps $60-70 billion annually.

But AI revenue doesn’t stop at API providers. Google Cloud’s $20 billion quarter is partly AI-driven. Microsoft’s AI business ARR grew 123% year over year. Salesforce, SAP, ServiceNow all embed AI into existing contracts. Count all AI-attributable revenue across the ecosystem and the number is probably $150-200 billion, growing fast.

That broader number makes the bear case harder to state cleanly. It doesn’t make it wrong. The infrastructure layer is spending $725 billion this year alone. Bank of America and Morgan Stanley project it crosses $1 trillion by 2027.

The optimistic read is that Anthropic going from $1 billion to $30 billion in fifteen months means the gap closes itself. Maybe. But growth at that velocity burns capital at the same velocity, and the data says most of it isn’t landing in enterprise income statements. Ninety-five percent of GenAI pilots still fail to produce rapid returns (MIT). Forty-two percent of companies scrapped most AI initiatives in 2025 (S&P Global). Eighty percent report no significant gains in top-line or bottom-line performance (McKinsey).

Nobody disputes that the models are useful. The question has always been whether useful pays for $725 billion a year. That question has a historical parallel: telecom in 2001.

What the Two-Layer Structure Means for You

When the correction comes, it won’t look like 2000. In 2000, everything crashed. In this cycle, the layers separate.

The infrastructure layer survives. NVIDIA will sell fewer chips. Hyperscaler capex will plateau or decline. But these companies have core businesses that print cash independent of AI. Google Search, Azure enterprise contracts, AWS, Meta’s ad revenue. They absorb the loss. The data centers don’t go dark, because unlike telecom fiber in 2001, they have immediate tenants.

The application layer gets shaken out. Companies at 568x revenue multiples, AI wrappers built on someone else’s API, pure-play model providers still burning cash. The ones that survive will be the ones that reach profitability before the capital markets tighten.

Nobody can stop first. If you’re the only one cutting capex, you “lose the race.” If nobody cuts, everyone bleeds. That competitive logic sustains the build-out far longer than the economics justify. It also means the correction, when it arrives, will be sharper than anyone spending $725 billion a year is planning for.

Build on the infrastructure layer. The compute is real, the cloud services work, and the pricing will only get cheaper as overcapacity materializes. But don’t bet your company’s engineering strategy on the application layer’s current pricing, business model, or even existence. The AI tools you rely on today may be sold, merged, pivoted, or shut down within 24 months.

The dot-com crash didn’t kill the internet. It killed Pets.com. The telecom crash didn’t destroy fiber. It destroyed the balance sheets of the companies that laid it. The pattern isn’t that bubbles kill the technology. It’s that they kill whoever borrowed to build it.

Who can actually pay?

P.S. If you want a deeper take on where the AI industry actually stands, I’d strongly recommend subscribing to Gary Marcus .

First of all, I love your style, attitude, and usually opinions. This time, however, I seem to be strongly in disagreement, especially in your comparison. The Dot Com bubble burned a lot of cash, yes, and the AI bubble is doing exactly the same. You are comparing apples to oranges, here, putting on the same line _net_ losses to a combined income which counts the same thing twice or more. Considering NVidia as an AI company is like saying that who sells bricks is in the construction business. It isn't, it's merely profiting from it. OpenAI is burning so much venture capital money that it's hard to track, but still you report it as a profitable company. I really don't know how this post came to be, but I'm confused. Still, I could totally be wrong about this: your posts are always interesting, and intellectual challenges like this post are the occasion to grow.

This is a fascinating comparison and presentation of the structural differences between the dot-com era and today.

However, I think this thesis relies on a hidden assumption: that AI compute costs and efficiency are static. If we look at the data from the last two years, the cost to achieve a fixed level of performance (like GPT-4 grade reasoning) has dropped by nearly 10x annually due to better architectures (eg. MoE), quantization, and hardware improvement. If the 'burn' at the application layer is dropping an order of magnitude every year, the 'squeeze' on the customer might be a temporary transition rather than a structural failure.