The $50 Billion Utility

Cursor is worth $50 billion. Nine months ago, it was paying Anthropic $650 million a year on $500 million in revenue. Every new user made the business worse. It took over $3 billion in funding and a model it didn’t build to fix that. The fix is the point.

Investors see $2 billion ARR and apply a software multiple. But Cursor isn’t software, nor is OpenAI, nor is Anthropic. The economics are inverted, and they stay inverted even as revenue grows.

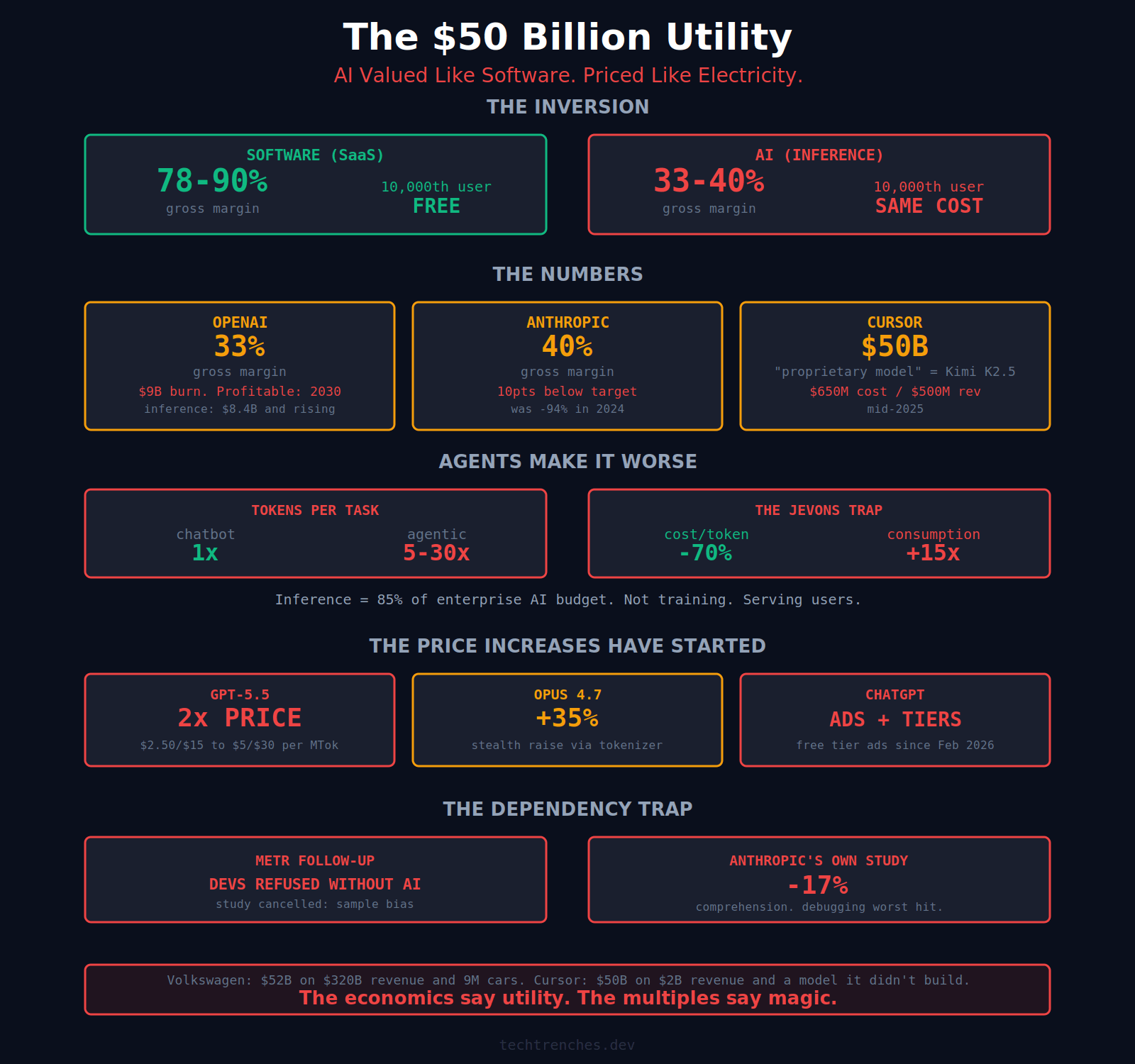

SaaS has one expensive phase: building. After that, the unit economics just sit there, compounding. Salesforce at 78%, Adobe at 90%, Atlassian at 85%. Growth doesn’t cost them almost anything.

AI didn’t make building cheaper, it moved the cost.

Queries run the model again. Tokens cost GPU time, memory, electricity. The 10,000th user costs exactly as much as the first. SaaS gets cheaper with growth. With AI, the bill just grows with you.

The industry doesn’t talk about it that way. Every company in the stack has a different metric. GitHub: lines generated. Cursor: PRs per sprint. Amodei at Dreamforce last October bragging that “90% of code at Anthropic is written by Claude.” None of them measure whether the software works. The metric measures the input. Nobody is measuring the output.

OpenAI generated $20 billion in revenue in 2025 and burned $9 billion in cash. Inference costs alone hit $8.4 billion, projected to reach $14.1 billion in 2026. Gross margin: 33%. Cash-flow positive: 2030. By then, cumulative losses will exceed $60 billion. At 30% margins on $20 billion revenue, paying that back takes decades. Anthropic looks better on paper: gross margin improved from negative 94% in 2024 to 40% in 2025, revenue grew tenfold. But 40% still fell 10 points below internal targets. The company lowered its own margin projection even as revenue exploded.

Cursor tells the clearest version of this story. Michael Truell’s company went from a $400 million valuation to $50 billion in 18 months, and the growth is real, which makes what follows worse.

But Foundamental calculated negative 30% gross margins in mid-2025. Hit $500 million ARR while paying $650 million to Anthropic. Reached “slight” profitability by launching what it called a proprietary model in November 2025. In March 2026, a developer found the model ID in the API response: kimi-k2p5-rl-0317-s515-fast. The “proprietary model” was Kimi K2.5, an open-source model from Beijing-based Moonshot AI, fine-tuned with reinforcement learning.

Even if it works, it doesn’t solve the problem. It moves the bill from Anthropic’s invoice to Cursor’s own GPU infrastructure. The inference cost per query doesn’t disappear because you’re running the model yourself. Enterprise accounts are now reportedly profitable. Individual developer accounts are not. The $50 billion valuation needs both segments to work. That was the fix for today’s product. Tomorrow’s product is more expensive to run.

And the Product Roadmap Makes It Worse

The industry’s answer to the margin problem is agentic AI. This is the story behind Cursor’s $50 billion, Devin’s $25 billion, OpenAI’s Codex. Agents are the product roadmap. Agents are also the margin killer.

A chatbot query hits the model once. An agentic loop hits it 10 to 30 times per task. Gartner’s analysis confirmed: agentic models require 5 to 30 times more tokens than a standard query. The pilot economics, calculated on single-query API calls, bear no relationship to the production economics of multi-step loops running thousands of times per day.

API costs fell 70% in early 2026. Token consumption rose 15x. Net AI spend goes up. Organizations that signed annual contracts in 2025 are paying 2 to 3x current market rates. The ones on consumption pricing are paying more than they budgeted because volume ate the discount.

KV cache, the memory structure that stores attention during generation, scales linearly with context length. Every byte for one user is a byte unavailable for another concurrent user. At 32K context, a single user’s cache approaches the size of the model weights. Double the context, halve your concurrent users. Inference is 85% of enterprise AI budget. Not training, not R&D, but serving users. Somebody has to pay for that.

So the Companies Are Raising Prices

In April 2026, both companies moved at once. Anthropic released Opus 4.7 at the same rate card as 4.6: five dollars input, $25 output. Unchanged. Except the new tokenizer generates up to 35% more tokens for the same text. Your prompt didn’t change, and your bill grew. Anthropic didn’t raise prices. They redefined the unit of measurement. A week later, OpenAI released GPT-5.5 and didn’t bother with subtlety. Input: $5 per million tokens. Output: $30. GPT-5.4 was $2.50 and $15. Doubled in one generation. The budget “mini” and “nano” tiers from 5.4 don’t exist for 5.5.

Nick Turley, head of ChatGPT: “Having an unlimited plan is like having an unlimited electricity plan. It just doesn’t make sense.” ChatGPT’s free tier shows ads since February 2026. A new $100 Pro tier was wedged between Plus and the $200 Pro in April. The staircase is being built: nerfing lower tiers, adding higher tiers, pushing users up. The pattern is familiar. Uber subsidized rides until drivers and passengers were locked in, then raised prices. Whether or not AI companies are following the same playbook intentionally, the sequence is identical. It only works if users can’t switch.

And Users Can’t Leave

METR, the AI evaluation lab, tried to run a follow-up to their 2025 developer study, but they couldn’t. A significant share of developers refused to participate if it meant working without AI tools.

Not refused the methodology, they refused to work without the tool.

Anthropic’s own January 2026 study explains why. Developers learning a new framework with AI scored 17% lower on comprehension tests than those learning without it. Debugging was worst hit. The study tested learners, not experienced developers, but METR saw the same pattern in seniors.

Last month, a mid-level developer on my team was asking Claude how to add sorting and pagination to a Microsoft API integration. Claude kept saying the API didn’t support it. The developer was ready to rewrite the entire integration layer, a 40-hour job. I checked the API myself. Sorting and cursor pagination worked fine on the endpoint he needed. Claude had been confidently wrong, and the developer never opened the documentation to verify. He trusted the tool over the source.

When Salesforce raises prices, companies evaluate alternatives. When AI coding tools raise prices, a growing share of users can’t easily switch to manual work. Juniors never built the skill, seniors lost the habit. The switching cost isn’t contractual, it’s cognitive. I’ve covered the burnout side in Human Cost and the skill atrophy in Comprehension Extinction.

In April 2026, OpenAI included text-embedding-3-small in a batch deprecation announcement. Hours later, they corrected it, the model stayed, but the panic was instant. RAG systems embed your entire knowledge base with a specific model. Every document, every vector. The vectors aren’t portable. Model disappears, you re-embed everything. Vector database rebuild, data ingestion again. For a million documents, that’s a five-figure bill.

Most of our clients run production RAG on OpenAI embeddings. The deprecation email meant one thing: their entire knowledge infrastructure sits on a model that a single API announcement can kill.

Inference is now a line item on your IT budget. Two years ago it didn’t exist. You don’t know how much it will cost. The vendor can change the model, the pricing, or the tokenizer at any time. You budget for a number that someone else controls. The obvious alternative is open-source models you host yourself. But that means you add infrastructure, ops burden, and another system to keep running. There isn’t a clean exit here, just a different kind of trap. So what breaks the cycle?

The Math

The bull case has three exits. None of them is working. Inference costs fall faster than usage grows. They haven’t: costs down 70%, usage up 15x. Companies build their own infrastructure. Cursor tried: a fine-tuned open-source model and billions in funding. Even if it worked, they still pay for every query on their own GPUs. OpenAI is spending $100 billion. This path is open to three companies on Earth. Prices rise until the economics work. GPT-5.5 doubled API prices in one generation. Anthropic stealth-raised through tokenizer changes. Turley is preparing users for the end of unlimited plans.

Cursor raised over $3 billion trying to fix the math. Whether it worked, nobody outside the company knows. The $50 billion valuation assumes it did, and that the rest of the industry can do the same. Users will pay, not because the value is there, but because the alternative is learning to code again without the tool. Most won’t.

None of these companies trade publicly. The $50 billion is what a group of investors in a room agreed to pay per share in a single round. No public market scrutiny, no quarterly earnings test. Cursor at 25x revenue, Anthropic at 40x, OpenAI at 42x, and public utilities trade at 3 to 5x.

Volkswagen is worth $52 billion. It makes 9 million cars a year on $320 billion in revenue. Mercedes-Benz: $57 billion. Real factories, real inventory, real profit. Cursor is worth roughly the same. It wraps API calls around a model it didn’t build on revenue that couldn’t cover the inference bill nine months ago.

The economics say utility. The multiples say magic.

I'm a number guy and I loved this one!

The scariest point you made is the reliance on AI by juniors and seniors (soon). It seems we created our own trap and there's no way out. Don't get my wrong, I love AI and everything it has to offer. I'd like to use it on my own terms rather than becoming a slave.

Isn’t the promise of Deepseek to achieve similar results at a fraction of the cost? Why hasn’t that taken off? Open AI and Claude both tell us how much better each iteration of their product is, but I don’t notice much difference personally.