Silicon Valley Eats the War

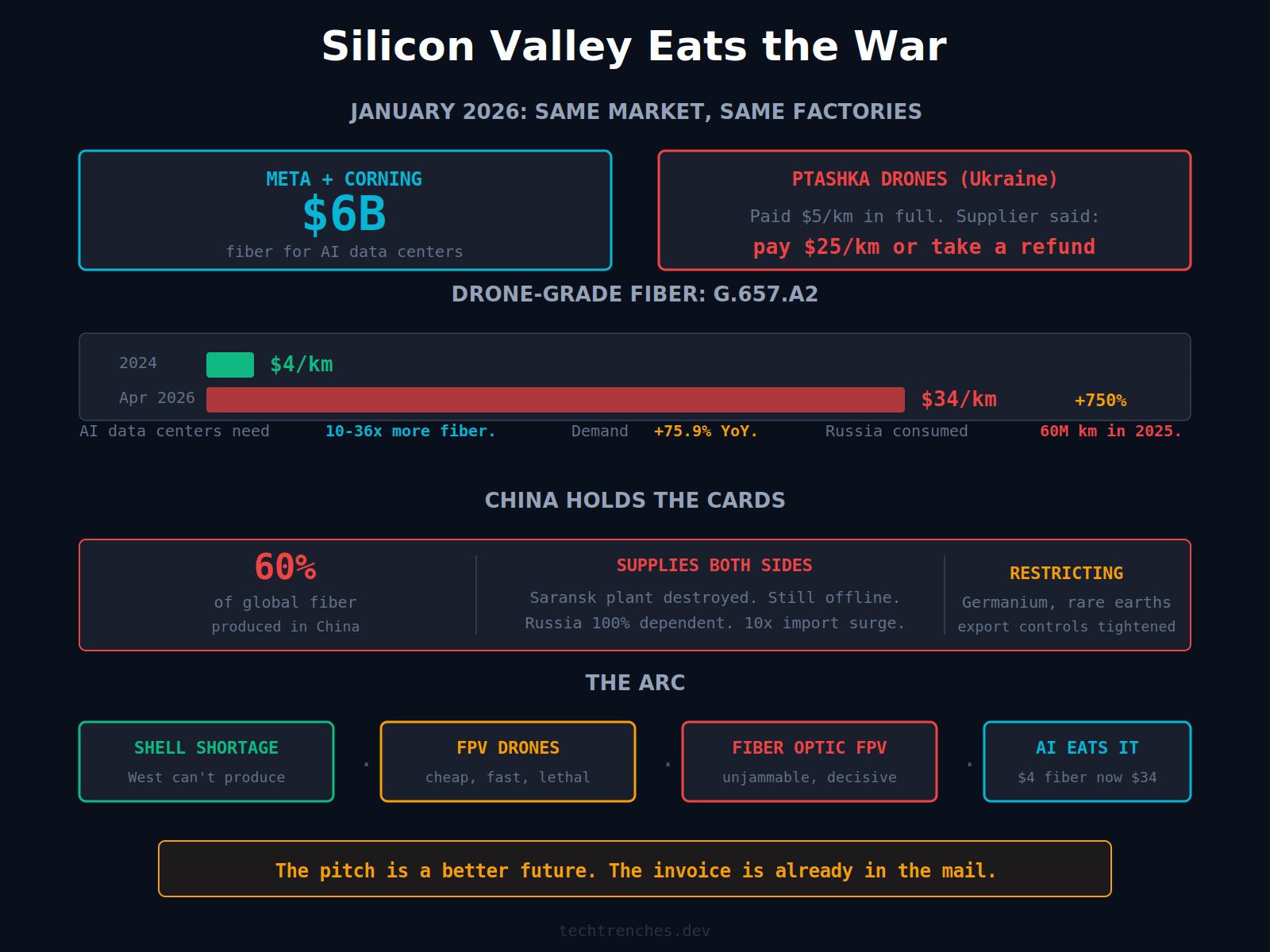

In January 2026, Meta signed a deal with Corning worth $6 billion for fiber optic cable. The same month, according to Ukrainian defense reporting, a drone manufacturer named Ptashka Drones paid in full for a fiber shipment from China at $5 per kilometer. The Chinese supplier came back and said: pay an additional $20 per kilometer, or take a refund.

Ptashka halted new orders entirely.

Both buy fiber from the same Chinese factories. One buyer builds AI data centers. The other builds weapons that are deciding a war. The mechanism is straightforward: when hyperscalers sign multi-year forward commitments worth billions, preform producers allocate draw capacity to those contracts. Spot supply shrinks. Spot prices spike. A Chinese trader with a $5/km order from a drone workshop and a standing commitment from a hyperscaler makes an obvious choice.

I wrote last month about how the West’s broken military industry created the shell shortage that nearly cost Ukraine the war. FPV drones changed that equation. Cheap, fast, lethal. They neutralized Russia’s artillery advantage. Then Russia put those drones on fiber optic cable at Kursk, and they became the single deadliest weapon on the battlefield. Today, AI is reshaping even that niche. Not on the front line. In the supply chain underneath it.

A Strand of Glass That Kills Tanks

Fiber optic guided drones are one of the defining weapons of this war. Replace the radio link on a standard FPV drone with a physical fiber optic cable that unspools during flight. The operator gets full-HD video through light pulses in the glass. The connection is completely immune to electronic warfare jamming. Both sides have poured billions into radio-frequency jammers. Fiber optic variants ignore all of it.

Ukraine produces over 50,000 fiber optic drones per month across 35+ manufacturers. Russia produces at least as many. Total FPV drone output on both sides is far higher, roughly 4 to 7 million per year each. But every fiber optic drone is a consumable munition. When it hits its target, the 10 to 20 km of G.657.A2 single-mode fiber it trailed behind is destroyed. The longest Ukrainian variant unspools 41 km in a single flight.

Russia alone consumed approximately 60 million km of fiber in 2025, up from near zero before mid-2024. That’s roughly 10% of total global production. Ukraine’s consumption adds to that total. Ukrainian drones now account for over 60% of strikes on Russian targets. NATO’s 2025 Innovation Challenge focused entirely on countering fiber optic drones.

The gap between the two sides is growing. Frontline operators estimate that Russia has shifted roughly 60% of its drone communications to fiber optic. Ukraine’s fiber optic drones make up just 15% of its total. Commander-in-Chief Syrskyi admitted in January 2026 that Ukraine is only “catching up.” Part of the reason is cost. And the cost problem didn’t start on the battlefield.

The Collision

The same fiber grades feeding drones are in accelerating demand from AI data centers. The data center customers have deeper pockets than any military procurement office on earth.

Corning reports that generative AI data centers require 10x more fiber than traditional facilities. Some estimates put it at 36x for GPU-dense racks. Global data center fiber demand surged 75.9% year-over-year in 2025, projected to jump from 5% of total demand in 2024 to 30% by 2027.

Supply can’t keep up. Fiber preform manufacturing requires 18-24 months to expand. At least one major US manufacturer has sold its entire inventory through 2026. Lead times for ribbon fiber approaching a year. Corning’s CEO reportedly stopped selling raw glass to other cable manufacturers in late 2025. China controls roughly 60% of global germanium supply and has been restricting exports since 2023, with further tightening in late 2024.

On the ground: G.657.A2, the drone-grade fiber, surged from approximately $4 to $34 per kilometer by April 2026. By May, frontline units reported paying $50 per kilometer. Multiple manufacturers report drone costs have roughly doubled, with the fiber spool now accounting for the majority of a drone’s price. Gedz Tech reported in March that the price jumped from $24 to $29 in two weeks. No signs of stabilization.

A Starlink terminal now costs less than a single 35 km fiber spool.

Ukraine’s Defense Procurement Agency cited two causes: the war itself and the civilian sector’s sharply increased consumption, primarily for data centers supporting AI. The war is the larger driver of G.657.A2 demand today. But additive demand in a market already at capacity is what breaks supply chains. Fiber is the sharpest example because the data is public and the victims are named. It’s not the only one.

Not Just Fiber

I wrote about the AI Silicon Tax in January. RAM prices jumped 187% because manufacturers reallocated to AI.

Chips are the same story at a different layer. Military systems rely on mature-node chips (90-300nm) that foundries deprioritize in favor of leading-edge AI silicon. TSMC is doubling advanced packaging for AI while legacy capacity stagnates, partly because of weak consumer demand, partly because the margins aren’t there. Today, Ukraine targets 4.5 million drones in 2025, requiring roughly 18 million motors. European component production can’t keep pace.

Copper is next. S&P Global quantified it in January: both AI and defense demand triple by 2040, while production peaks in 2030. Ten million metric ton deficit. There’s no spot market fix for that.

Rare earths are a single point of failure with a flag on it. China controls 70% of production and 90% of processing. The same neodymium in F-35 engines goes into data center cooling motors. In October 2025, Beijing tightened export controls further.

Energy follows the same pattern. US data centers consumed 183 TWh in 2024, more than Pakistan’s annual demand. Wholesale electricity prices have risen 267% near data center hubs like Northern Virginia, where defense contractors also compete for grid capacity. When AI firms lock up long-term power purchase agreements, industrial users further down the priority list pay more or wait.

Pull any thread and you end up in the same place. US broadband expansion targets are already slipping because the same fiber shortage is hitting telecom providers who can’t get cable for rural deployments. It reaches anywhere that needs physical infrastructure and can’t outbid a hyperscaler. And nearly all of it runs through one country.

China Holds the Cards

China supplies both sides. That’s not a secondary detail. It’s the architecture of the problem. China produces 60% of global fiber. The same supply chain feeds Russian and Ukrainian drone manufacturers.

After Ukrainian drones struck Russia’s only domestic fiber plant in Saransk in spring 2025, which had produced approximately 4 million km per year, Russia became 100% dependent on Chinese imports. A year later, the plant still isn’t operational. Imports jumped tenfold. Chinese suppliers responded by demanding 100% prepayment.

Ukraine faces the same dependency. Most fiber reaching Ukrainian manufacturers originates in China, entering directly or through European intermediaries. Some companies have diversified to European sources, but domestic Ukrainian production would require hundreds of millions in investment and several years to build. Zelensky signed laws in 2025 canceling VAT and duties on fiber drone components. The government is discussing state procurement of fiber as a strategic raw material.

These are mitigation measures against structural math. Russia alone consumed 60 million km last year, as I said before. Ukraine’s consumption adds to that. AI data center demand grows at 75%+ annually. You can’t procure your way out of a preform shortage. But the AI industry isn’t trying to. It doesn’t see the shortage the same way.

The Cost We Don’t See

The product announcements read like software releases. Model update. New API. Benchmark. The supply chain underneath reads like a mining report.

The pitch is a better future. The invoice is already in the mail. Fiber prices double and Ukrainian drones get more expensive to build. Energy costs surge near data center hubs and industrial production gets squeezed. Rare earth export controls tighten and defense supply chains break.

How much copper went into the last Virginia data center that could have wound an electronic warfare system instead? The fiber in GPU clusters and the fiber guiding drones into trenches share the same upstream supply chain: same preforms, same drawing towers, same raw materials. The semiconductors running recommendation engines compete with the chips Ukraine needs for drone motors.

It’s happening on a planet where the same raw materials are fighting a war. Defense analysts and commodity traders track it. It doesn’t routinely reach the people making AI investment decisions.

Have you seen supply chain competition between AI and other industries in your work? Reply and let me know.

If this analysis matters to you, forward it to someone in defense procurement or AI infrastructure.

Data centers are wildly overbuilt but not a complete waste. The Ukraine war is complete waste.