When Your Vendor Becomes Your Competitor: AI’s $5.5B Confession

Sam Altman and Dario Amodei spent two years predicting AI would displace much of the workforce. Both hedged with talk of augmentation and regulation, but displacement was the headline, and it shaped enterprise expectations, investor theses, and hiring decisions across the industry.

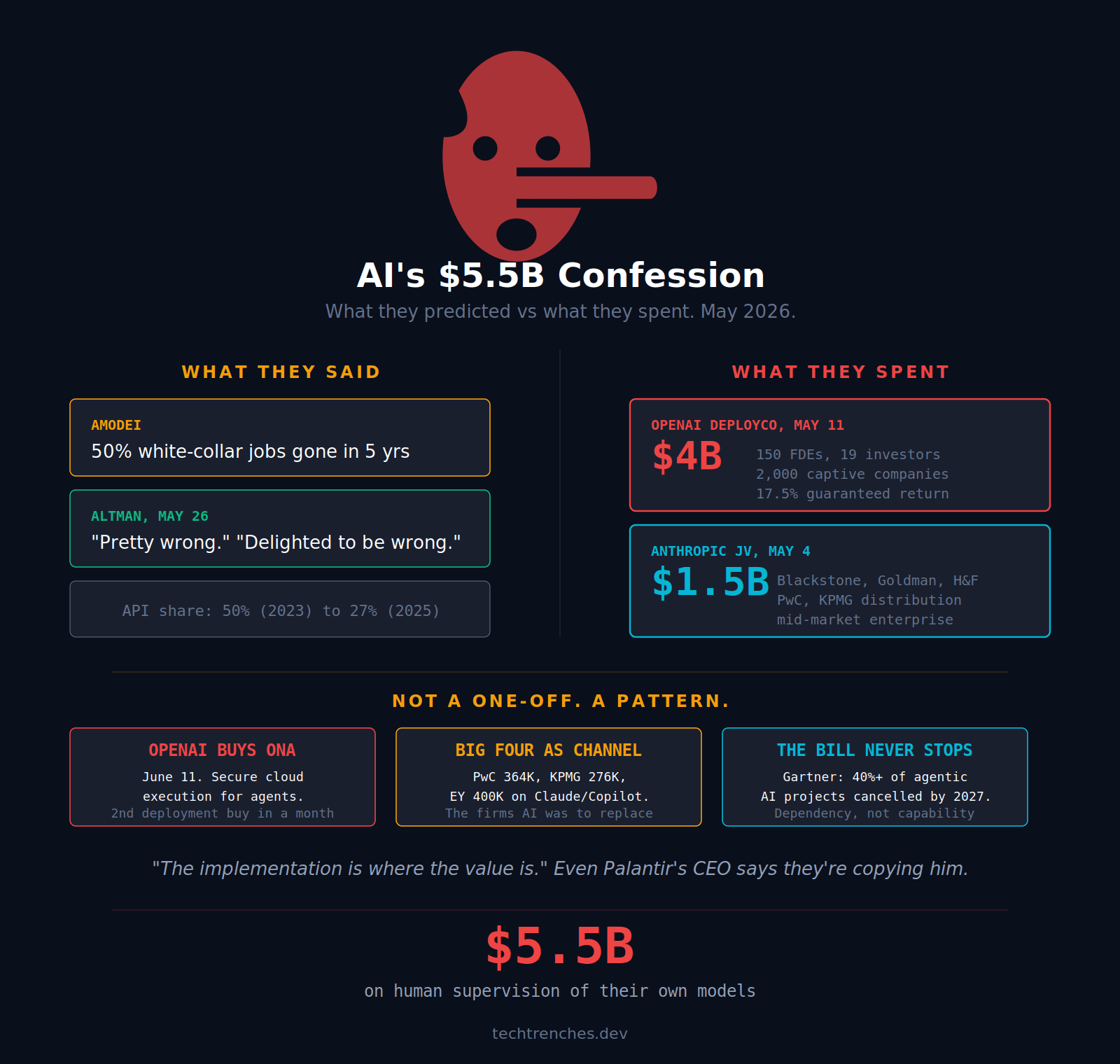

Then, in May 2026, OpenAI launched a $4 billion company that sells human supervision of its own models. To the same enterprises. For the same work thousands of independent engineering firms were already doing. Anthropic did the same thing a week earlier, quieter, for $1.5 billion.

They didn’t build a better model. They built a services firm. And the $5.5 billion they spent is the clearest admission yet that enterprises can’t deploy AI without humans holding their hand.

The Vendor Ate the Ecosystem

OpenAI’s Deployment Company launched May 11 with $4 billion from 19 investors led by TPG, including Goldman Sachs, McKinsey, and Capgemini. Its first hire: 150 forward-deployed engineers from Tomoro, a London consultancy acquired the same day.

Forward-deployed engineers sit inside your company and make AI do what the demo promised. Palantir pioneered the role in the early 2010s because its software didn’t deploy itself either. The model works. Palantir’s stock returned over 1,200% since 2020 on exactly this premise: enterprise software needs permanent human support.

So copying Palantir isn’t the problem. The problem is that OpenAI’s CEO spent two years saying the model makes this work obsolete, then built a $4 billion company to do it.

The structure gives away the confidence level. DeployCo’s investors collectively sponsor 2,000+ businesses, a captive market built into the cap table, and OpenAI guaranteed them a 17.5% annual return. That’s standard private-equity plumbing, except the asset generating the yield is a supervision business, not a software license.

Every AI services firm that built on OpenAI’s API now competes against a subsidiary of its own vendor, one that sees the model roadmap first and has thousands of clients pre-sold through the cap table. Axios’s Dan Primack caught the irony: McKinsey and Capgemini invested in DeployCo while competing with it. They funded their own disintermediation, or bought a hedge against it. Either way, they’re inside the tent.

AWS and Salesforce competed with their partners too, but offered margin sharing and co-sell programs to keep the ecosystem alive. DeployCo is built as a competitor, not a platform. OpenAI went from tool vendor to rival services firm in eighteen months.

Then it kept going. A month after DeployCo, OpenAI acquired Ona, which runs AI agents securely inside an enterprise’s own cloud. One acquisition makes a product. Two makes a pattern. OpenAI is buying its way into the deployment layer because the models alone don’t land there.

The Middleman They Were Supposed to Kill

Anthropic didn’t build its own engineering arm. It rented everyone else’s.

PwC signed on May 14: Claude across 364,000 employees, 30,000 to be certified. KPMG followed five days later with “Digital Gateway Powered by Claude” for 276,000 people in 138 countries, plus a product for modernizing IT at private-equity portfolio companies.

These are auditing firms. Tax prep, compliance, M&A advisory, the exact white-collar work every pitch deck promised to automate. Instead of being replaced, they became the sales channel. Enterprises don’t trust Claude. They trust KPMG. So KPMG stamps “Powered by Claude” on its existing workflow and bills both ends: Anthropic for distribution, clients for the supervision.

You could argue this is augmentation working as designed, and you might be right. PwC reported up to 70% faster delivery on client work. But augmentation isn’t what got the funding and the keynotes. Displacement was the pitch, and the gap between that pitch and a Big Four distribution deal is the whole story.

The model didn’t cut out the middleman. It entrenched it.

The pattern is industry-wide. By the end of May, every major lab had bought its way into someone’s services arm: EY went with Microsoft, Google funneled $750 million into Accenture, Deloitte, and Capgemini. Embedded enterprise engineers aren’t new; Microsoft and AWS have fielded them since 2017. What’s new is the model vendors muscling into the same work, on top of a services layer that already existed.

What all this money buys is a human signature on a risk assessment. Confidence-as-a-service, priced like infrastructure.

And the bill never stops. When the deployment never gets cheaper from one engagement to the next, you didn’t buy a capability. You bought a dependency. Forward-deployed engineers are the invoice for making AI real.

The Contradiction That Funds Itself

Back in 2024, Amodei predicted 50 million genius-level AI entities and half of white-collar jobs gone in five years, then doubled down in a 20,000-word essay in January 2026. I took it apart then: the knowledge required to supervise AI is the same knowledge that makes you irreplaceable.

Four months later, the money confirmed it. While Altman’s people were buying a London consultancy, our CTO was staring at a queue of vibe-coded apps that HR, PMs, and even our own CEO had built and now wanted shipped to production. That queue is the real shape of AI in the enterprise: not replacement, but a backlog of half-working software that needs a human to make safe. On May 26, Altman told a Sydney audience he’d been “pretty wrong” about AI and jobs, and said he was “delighted to be wrong.” More honesty than most CEOs offer. But his company had spent $4 billion two weeks earlier, and that says more than any interview.

Then Amodei went further. In a June policy essay, he proposed that if AI permanently kills demand for labor, governments may need universal basic income funded by taxes on AI companies. Read that again. The same person, the same company that has spent eighteen months selling labor replacement now wants a tax-funded safety net for the moment that replacement lands. He’s pricing in the cleanup before the spill. So the same month Anthropic spent $1.5 billion hiring humans to deploy its models, its CEO floated paying the displaced out of a tax on the firms doing the displacing.

Either way, the math doesn’t reconcile. If the models replace workers, you don’t need 150 engineers inside client offices and four Big Four partnerships. If they don’t, stop writing 20,000-word essays about the country of geniuses. Pick one.

Lay the receipts in order and the three-week corridor speaks for itself. May 11, OpenAI launches its deployment company. May 14, PwC signs. May 19, KPMG follows. May 26, Altman says he was wrong about replacement. June, Amodei proposes a tax to clean up the replacement. The walk-backs and the checkbook were running on the same calendar.

The market already picked. OpenAI’s enterprise API share slid from 50% to 27% in two years while Anthropic took the lead. That slide is the motive. When the model stops being a differentiator and the API revenue follows it down, you wrap the model in people and sell the bundle, because a services contract is stickier than an API key. DeployCo is the answer to a losing API war, not a strategic flourish. Even Palantir’s Alex Karp, whose platform competes directly, called the Tomoro deal “a complete farce” and an attempt to copy Palantir. “The implementation is where the value is,” he said.

When the company that invented the playbook says you’re copying it badly, the model was never the moat.

What This Looks Like from the Trenches

We sell this exact service, at a fraction of $4 billion.

A client calls because someone on their team vibe-coded an internal tool with ChatGPT, and leadership wants it in production. Nobody knows if the API keys are exposed, whether data leaks outside the VPC, or how to enforce compliance on code no human wrote. They need an engineer to audit it, fix it, and sign off that it won’t detonate in production.

The queue isn’t hypothetical. Our DevOps team built dedicated infrastructure just for it: SSO, automated provisioning, the whole path from someone’s laptop to a managed environment.

OpenAI now sells that same work, with insider access to the model, a captive pipeline of thousands of companies, and a brand enterprises trust more than any independent firm. Your vendor is your competitor, with funding you can’t match, a roadmap you can’t see, and a client base you can’t access.

For buyers, the tradeoff is real. DeployCo’s engineers are good; Tomoro had real clients and real deployments. But the firm that already knows your infrastructure and your edge cases just lost its information edge to your vendor. And 150 engineers spread across thousands of portfolio companies run thin fast.

The keynote is free. The $5.5 billion is the honest number, and it just built the most expensive human-supervision layer in enterprise history.

If Altman and Amodei spent two years telling the world that humans aren’t needed, they shouldn’t be surprised when the humans they’re now competing against take it personally.

Excellent piece. I had not heard of this before.

I am intrigued by the bit of insight you have included into the DevOps services you use internally and also market. With having to dissect and fix vibe-coded apps, I'm curious on your general impression of the code quality and maintainability. If you don't mind a couple of questions: Do you get into refactoring overall, or is your goal just to make sure the code not brittle and insecure? And, to what extent do your workflows utilize agentic coding tools?

Probability of error in LLMs follows a power law. You can not automate sh#t with those machines. You need EXPERT in the loop.

I saw many consultancy firms consulting

in the past. In the best case those forward deployed engineers are going to be overworked junior guys that start their career there just for their CV and abandon the firm when they are burn out before been 30 years old. In the worst case, these guys are not going to be engineers. They are going to be agent operators. In any case, salaries will go down. The final goal for which the current developers are so devotely helping to happen.