China Built the Grid Under the AI War

Gary Marcus has been calling the moment the US AI industry starts to break, and a fresh round of cheap Chinese open models is, to him, the evidence it has arrived. His case is three years old and it has not changed: no moat, free copies, prices to zero, and eventually the trillion-dollar IPOs stop penciling out. The only part he updates is the evidence. He is right about all of it. He is also looking at the wrong floor. The margin collapse he describes is the symptom. The disease is physical, and it sits a layer below the price war he is watching.

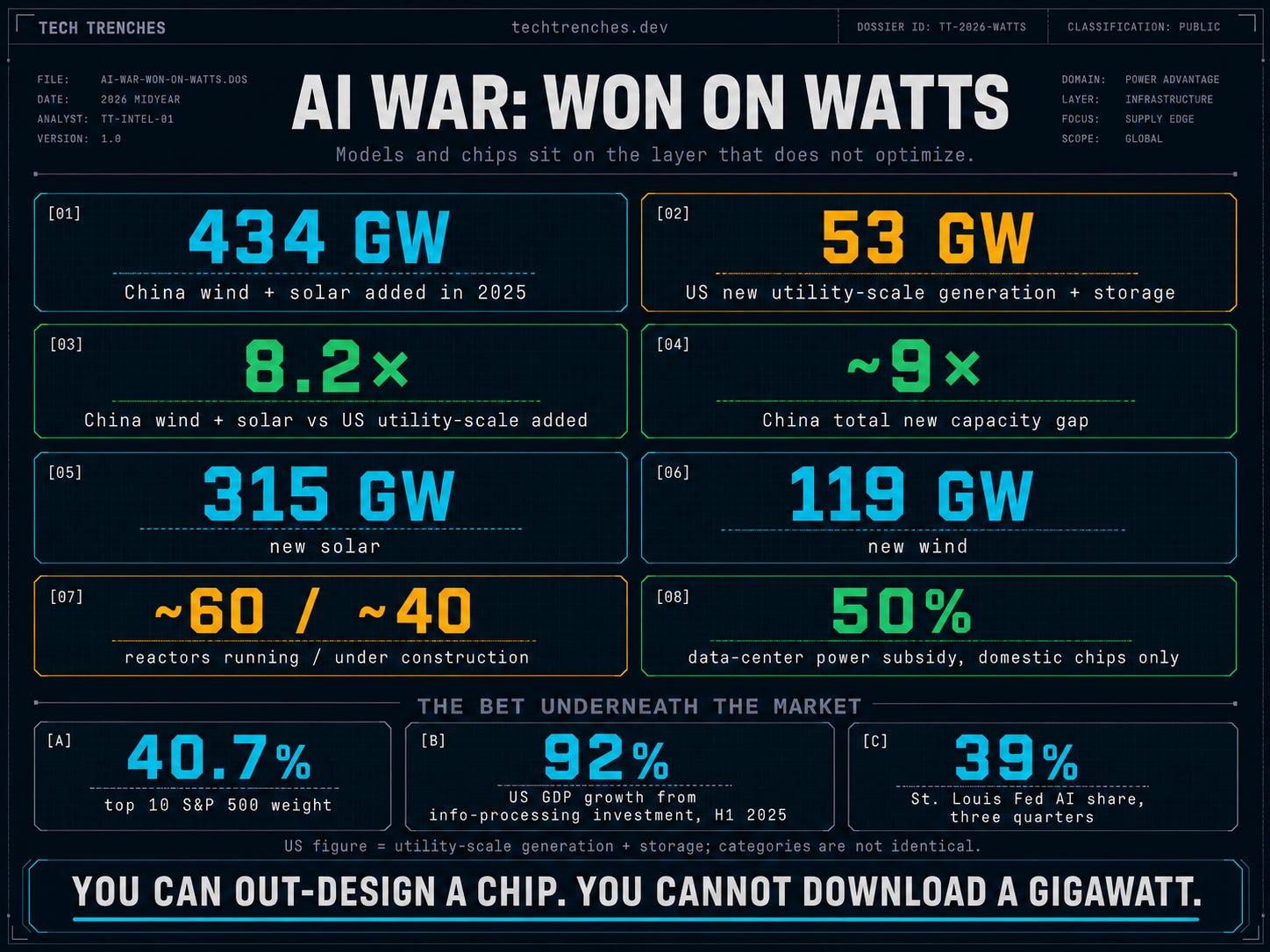

In 2025 China added 434 GW of wind and solar. The United States added 53 gigawatts of new utility-scale generation and storage. Those are not the same category, and I am not going to pretend a gigawatt of Chinese nameplate solar is a delivered gigawatt wired into a data center. The claim underneath is narrower and harder to wave away: one country is building enough capacity to treat power as a substitute for better chips, while the other is adding capacity into a grid that still cannot connect it fast enough.

Chips Have Shortcuts. Power Doesn’t

A chip deficit has shortcuts. Huawei just proved the crudest one, packing roughly five times as many mediocre Ascends into a rack-scale system until a single superior Nvidia die stops being the only route to frontier compute. Tighter code and smarter architecture are the quieter versions of the same move. Each one buys its way around the chip by spending more power.

A power deficit has no shortcut. New generation, new lines, new substations all take years and physical construction. I spent four years working through Russian strikes on the Ukrainian grid, and the lesson that stays with me is simple: electricity sits under everything else. When it goes, the models and the chips and the funding rounds are worthless at the same instant.

That is the asymmetry the whole race turns on. One side can buy its way around a worse chip by spending power it has in surplus. The other side cannot buy its way around a grid it has not built.

What China Poured

China spent the year on the side of the asymmetry that cannot be optimized away. Its energy administration reported 315 gigawatts of new solar and 119 of wind, both annual records, pushing wind and solar past thermal power in the national installed base for the first time. Chinese industrial power runs slightly higher per kilowatt-hour; price was never the advantage. Panels and turbines go up by the trainload, and the country has far fewer independent actors with the standing to keep a prioritized project stuck. The same system that green-lights a national project cannot stop a useless one, so China will pour concrete for data centers that never fill. It wastes the resource it has, not the one it lacks. The buffer does not rest on panels alone: the same year brought nearly 40 reactors under construction and a growing thermal base beneath the renewables, firm power that runs whether or not the wind blows.

It is the electric-vehicle script, rerun. A decade of subsidies handed BYD and CATL the global market, and a Stanford analysis found China kept 92 percent of the welfare gains at home. The same instruments now point at compute. Local governments in Gansu, Guizhou, and Inner Mongolia cover up to half the bill for data centers, on the condition they run on domestic chips rather than Nvidia. A draft national computing plan, reportedly worth nearly $295 billion, would mandate that 80 percent of its chips be domestically produced.

The mandate is the part that should hold Washington’s attention longer than any benchmark. Nvidia, an American company, spent the year trying to sell into China and mostly failing, because Beijing told its largest firms to stop buying. The country’s internet regulator barred ByteDance and Alibaba from purchasing the China-specific parts Nvidia designed for exactly that market. Jensen Huang flew to Beijing, lobbied in Washington, and watched a market that once supplied a fifth of his data-center revenue produce, in his own CFO’s words, no revenue at all. When the world’s most valuable chipmaker is the supplicant, and the buyer keeps choosing its own slower silicon over a discount on better hardware, the dependency runs the opposite direction from the one everyone assumed.

China’s AI Plus directive, issued by the State Council in August, frames AI around labor shortages, dangerous work, and upgrading existing roles rather than deleting them. I am quoting policy, not proven outcomes. It subsidizes the power, builds the chips, and treats AI as a tool.

I am Ukrainian. China is a direct ally of the country trying to kill mine, and I have no warmth for it whatsoever. Hatred is not an analytical method. I have spent four years watching what happens to people who underestimate a competent adversary. China is doing this part right. Refusing to see it would make me a worse analyst.

America Built a Position

Set against China’s poured concrete, American capital spent the same window building compute on top of a physical layer it does not control. By the end of 2025 the ten largest companies in the S&P 500 made up 40.7 percent of the index, a record, with Nvidia the heaviest single weight since the data begins in 1981. The four largest hyperscalers guided to roughly $725 billion in 2026 capital spending, more than four times the entire US energy sector’s capital spending, on hardware that depreciates in a few years. I traced that buildout in detail elsewhere.

Jason Furman, who chaired the Council of Economic Advisers, calculated that investment in information-processing equipment and software accounted for 92 percent of US GDP growth in the first half of 2025, against four percent of the economy. He added the honest caveat that the counterfactual is not zero, since cheaper power and rates absent the boom would have lifted other sectors, maybe halving the effect. Even halved, a single category carrying 40 percent of national growth is an economy wired to one bet, and one financed increasingly on debt.

Dario Amodei, who runs the most financially cautious of the frontier labs, told an interviewer in February that being “off by a year” on the growth rate, or growing 5x a year instead of 10x, is enough to “go bankrupt.” When the careful one says a one-year forecasting miss can bankrupt a frontier lab, it says something about what the reckless ones leave unsaid. The same industry now cuts headcount to fund the chips while forecasting the displacement that spending will cause. Beijing’s policy points AI at the jobs nobody can staff. The American frontier, in practice, points it at the jobs people already hold.

The bet also runs into the same wall the rest of the buildout keeps hitting. Power. The US added capacity at a record pace of its own in 2025 and still cannot connect it fast enough. I have written before about how the grid became the hard ceiling nobody priced into the spreadsheets.

Europe Published a Strategy

There is a third party in this race, and it is the one that clarifies the other two. Europe has no frontier AI chip at scale, no hyperscaler comparable to the American four, and no frontier lab at their level. Its most advanced chips are Nvidia’s, fabricated at TSMC and Samsung, and its one indispensable asset, ASML, makes the machines that make everyone else’s chips, not a sovereign stack of its own. US providers run about 70 percent of European cloud. Europe’s answer, delivered in June, was a sovereignty package: directives, a sequel to the chips act, a target to triple data-center capacity in five to seven years, funded mostly by private capital it admits it does not have. The target deserves the trust its last one earned. When Ukraine needed artillery, the EU promised a million shells in a year against production that ran at a third of that, and delivered late. China poured concrete and America placed a bet. Europe published a directive about doing one of them someday. It never fielded a side, and that is the only reason it cannot be said to have lost.

Where the Lead Actually Is

The model gap, the thing the West still tells itself it owns, is real but narrowing, and it is narrowest exactly where the work happens. On Artificial Analysis’s index of general intelligence, Zhipu’s GLM-5.2 scores 51 and leads all open-weight models, within striking distance of the proprietary frontier. But in Morph’s vendor-score aggregate for SWE-bench Pro, a coding and agentic benchmark closer to what engineers actually ship, Claude Opus 4.8 leads GLM-5.2 by about seven points, 69.2 to 62.1, while the open model costs a fraction as much to run. That is a gap a research lab notices and a working engineer often does not. For a growing share of ordinary coding and text work, which is most of what anyone runs, the remaining gap is no longer commercially decisive. And the Chinese models carry an advantage no benchmark scores: they ship as open weights. You can run Qwen or GLM on your own hardware, fine-tune it, and deploy it with nobody’s API in the loop. A Western frontier model is a lever the vendor still holds. Released Chinese weights are a lever nobody can pull back.

The chip gap is real. Huawei’s fabricator, SMIC, is stuck around 7nm while TSMC builds Nvidia’s parts two or three nodes ahead, and policy cannot fix a lithography line on any useful timeline. What Huawei did instead was stop fighting on the die and start fighting on the rack. Its CloudMatrix cluster packs five times as many Ascend chips as Nvidia’s flagship server and matches it on aggregate compute and memory, burning nearly four times the power to do it. That trade ruins you where electricity is scarce. In the regions China has deliberately provisioned with excess generation and subsidized power, that penalty becomes one the state is willing to absorb. One cluster design does not solve China’s semiconductor industry. It is enough to keep domestic frontier-scale training strategically viable while Beijing pushes Nvidia’s local share toward single digits by declining to buy. The hardware question is being answered at the rack, not yet at the fab, and that is the layer where the training runs.

An American data center’s power waits on an interconnection queue, a regulator, and a dozen parties who can each say no. A Chinese one waits on a ministry that has already said yes. You can out-research a command economy on models and out-design it on chips. You cannot out-build it.